As of 1 July 2025, super funds with balances over $3 million will be taxed at 30%. Here’s what the change actually means.

What’s the deal with the new ‘30% tax’?

The Albanese Labor Government has struck a decisive compromise in its desire to rein in the cost of tax concessions on large superannuation balances. Treasurer Jim Chalmers has recently announced that the taxation on earnings from superannuation balances in excess of $3 million will double to 30% as of 1 July 2025. The existing 15% rate on accumulation funds will continue for all super balances below $3 million.

Right now, if you have a super balance of over $3 million, you are taxed at the current concessional rate of 15%. Once you turn 60, the tax rate falls to zero for earnings funds in the pension phase with a Transfer Balance Cap (TBC) of currently $1.7 million limiting how much can be moved into the pension phase.

However, as of 1 July 2025, the concessional rate will be doubled. While the Prime Minister and Treasurer say that this will only effectively impact 80,000 accounts or 0.5% of the population, we think it is important that every Aussie understands what this change means for them and their families.

The Treasury Fact Sheet here holds a surprise in the way the extra tax will be calculated:

- The Australian Tax Office will issue tax liability notices to individuals in the 2026-27 Financial Year

- Earnings will include unrealised capital gains (or losses) in the calculation

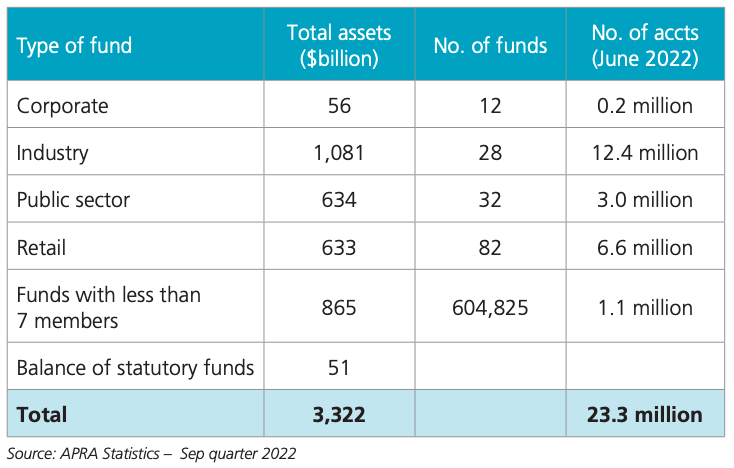

Data in table sourced at: ASFA

Circulating freely are the fears of a hard cap incentivising rich Australians to remove their nest egg money from super, or the imposition of tax at the top personal marginal rate. Nevertheless, these have yet to be realised, and the delay until after the next election gives time for consultation and modification.

Why is the Government doubling the tax?

The Government’s main argument is that Australia is $1 trillion in debt and this tax rate change can help pay it off. The debt is due to a combination of factors – such as government spending, lower tax revenues and external economic factors. The COVID-19 pandemic, in particular, has had a significant impact on our economy, resulting in reduced tax revenue due to lower economic activity and increased government spending on measures like economic stimulus packages and healthcare costs. Meanwhile, trade tensions with China, our largest trading partner, have resulted in reduced export revenues, further contributing to our national debt. That being said, government debt is a common tool and is acceptable, so long as the Government is effectively managing debt levels and ensuring sustainable economic growth/inflation.

The Albanese Labor Government has reiterated that the purpose of super is to ensure that Australians have a comfortable retirement and that those with super balances over $3 million have beyond what is necessary for this. When the Prime Minister was told that 17 people had super balances of over $100 million, he said, “it [would] be irresponsible to not take any action.”

By doubling the concessional tax rate on super balances of over $3 million, the change will raise up to $2 billion in its first full year of operation. This will increase over time as the $3 million threshold will not be indexed to rise with inflation; the reasoning for this is to ensure the super system remains sustainable.

How will the new tax work?

Treasury’s Fact Sheet here explains in detail how the tax will be calculated, based on the increase in individual balances rather than imposing a tax on a super fund.

Each individual will be assigned a Total Superannuation Balance (TSB). Those with over $3 million at the end of a financial year will be subject to a tax of 15% on earnings. The earnings are calculated using the difference between the TSB at the start and end of consecutive financial years, adjusted for withdrawals and contributions.

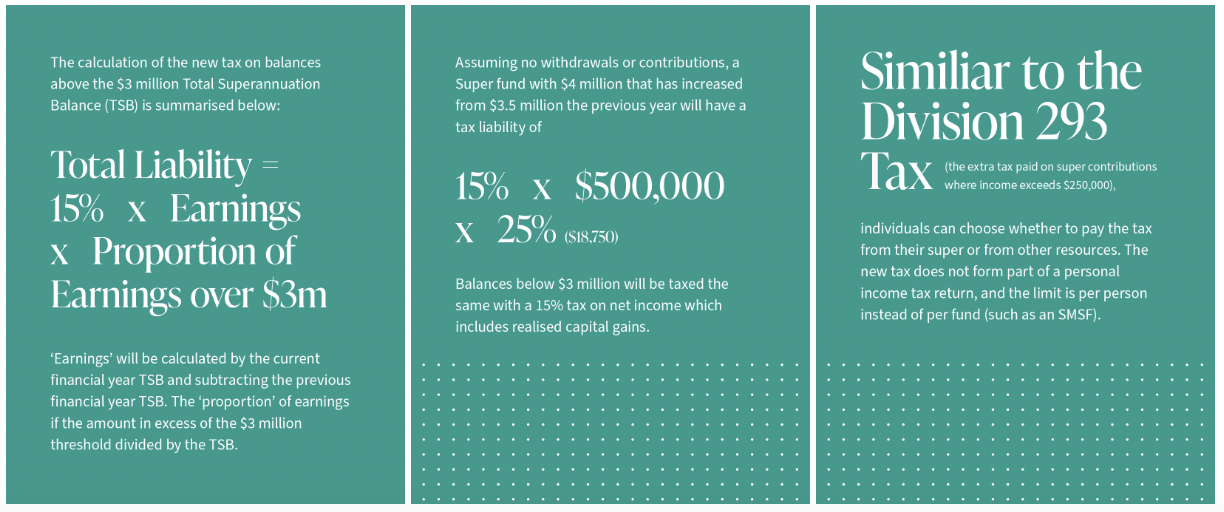

The calculation of the new tax on balances above the $3 million TSB is summarised below:

Tax Liability = 15% x Earnings x Proportion of Earnings over $3 million

‘Earnings’ will be calculated by the current financial year TSB and subtracting the previous financial year TSB. The ‘proportion’ of earnings if the amount in excess of the $3 million threshold divided by the TSB.

To bring it together, assuming there are no withdrawals or contributions, a Super fund with $4 million that has increased from $3.5 million the previous year will have a tax liability of 15% x $500,000 x 25% ($18,750).

Balances below $3 million will be taxed the same with a 15% tax on net income which includes realised capital gains.

Similiar to the Division 293 Tax (the extra tax paid on super contributions where income exceeds $250,000), individuals can choose whether to pay the tax from their super or from other resources. The new tax does not form part of a personal income tax return, and the limit is per person instead of per fund (such as an SMSF).

The eye-opener here is that earnings include unrealised gains. Total Superannuation Balances will be tested for the first time on 30 June 2026 with tax liability notices issued in 2026-27.

How accurate will the asset valuations be?

Here lies the main drivers for the call to reconsider the policy. As with the taxing of unrealised gains, the issue of how unlisted assets are revalued becomes a lot more problematic. Assets in the listed space such as illiquid securities are also affected as such stocks are usually traded in small volumes, meaning prices can vary widely depending on whether a bid or offer is hit at the last trade.

The added complication with this new tax is that members will now pay tax on the values of their super assets, intensifying the focus on how assets are valued.

Will the change really affect 80,000 accounts?

There are already reports that are finding this to be untrue. Because the $3 million threshold will not be indexed to inflation, it’s essentially a real cap of $1 million in today’s dollars. This means that if you are in your 30s and 40s right now, you could also be affected when you retire at 65, according to the FSC. This number is reportedly more like 500,000 accounts than 80,000.

So, should I pull back on my savings for retirement then?

Definitely not as many Australians rely on their super balances to fund their retirement. However, you should examine whether your super is future-proof such as whether there are better contribution strategies you could use or whether you could equalise your super as a couple. Other options to look into could potentially be SMSFs, cashing out the amount in excess of $3 million where a Condition of Release has occurred, moving the money into a Discretionary Family Trust (DFT) which already has a company listed as a beneficiary, and rebalancing your super.

How do we rebalance our super and why should we do it?

The $3 million threshold is an individual threshold so couples may wish to investigate methods to balance accounts between spouses. Two such methods are:

- Super splitting where contributions to super can be split with your spouse, including but not limited to employer contributions and salary sacrifice contributions.

- After reaching a condition of release (after age 60), you may consider withdrawing funds from one spouse’s super and re-contributing to the other spouse’s super as a non-concessional contribution. Current caps are $110,000 per annum or $330,000 using a bring forward arrangement.

However, it’s important to note that there are other factors to consider when making super contributions, such as contribution caps and your overall financial goals. So while the change doesn’t come into effect until 2025, it might (definitely) be in your best interests to start planning to make the most of your super and optimise your tax benefits.

We highly recommend setting an appointment with a Green Associates Financial Planner and Adviser to determine the best approach for your specific circumstances. Call 1300 815 921 or email info@greenassociates.com.au to get started!